Request for Comments – Proposed Public Interest Rule Amendment – Directed Indications of Interest – Cboe Canada Inc.

OSC staff (Staff) is publishing today a notice (Notice) of Proposed Public Interest Rule Amendment and Request for Comments from Cboe Canada Inc. (Cboe Canada) regarding the introduction of a new order type to Cboe Canada's MATCHNow trading book (MATCHNow) called Directed Indication of Interest (Directed IOI).

A full description of the proposed functionality and Cboe Canada's submissions of its rationale and expected impact are in the Notice. While comments are requested on all aspects of the Notice, for the purpose of responding to Staff's request for specific comments below, Staff notes the following aspects of the Directed IOI functionality.

As described in the Notice, a buy-side institutional firm that has direct electronic access to MATCHNow (Sponsored User) must be an existing client of the dealer member (Member) to be able to receive Directed IOIs from that Member. The Member can then choose which Sponsored User(s) will receive a particular Directed IOI message. In addition, the Sponsored User can filter the messages it receives based on certain types of liquidity (e.g., by specific Member(s) and the nature of liquidity that the Member's Directed IOI represents, including client agency, dealer proprietary or market making). Orders generated through the Directed IOI functionality do not interact with other orders in the MATCHNow order book.

In other words, the Directed IOI functionality allows certain market participants to choose the counterparties and certain attributes of orders with which they wish to interact and ultimately trade against. It does not allow all market participants the opportunity to trade against all orders, but rather enables certain participants to interact based on pre-existing relationships. Directed IOIs will be subject to a minimum notional threshold of $100,000 in value.

Staff notes that as part of the Notice, Cboe Canada has not proposed to institute an automated compliance mechanism for monitoring messages transmitted between Members and Sponsored Users in the context of Directed IOIs.

Staff request for specific comments

The "fair access" requirement in section 5.1 of National Instrument 21-101 Marketplace Operation states that a marketplace must not unreasonably prohibit, condition or limit access by a person or company to services offered by it. It also states that a marketplace must not

(a) permit unreasonable discrimination among clients, issuers and marketplace participants, or

(b) impose any burden on competition that is not reasonably necessary and appropriate.

Question 1: In your view, is the proposed Directed IOI functionality consistent with the fair access requirement?

Question 2: Would users of Directed IOIs have an informational advantage over other market participants since they would have information, including the nature of the counterparties, that is not available to other market participants?

Submission of comments

Comments on the Notice should be in writing and submitted by November 25, 2024 to:

and to:

Comments received will be made public on the OSC website. Upon completion of Staff's review, and in the absence of any regulatory concerns, notice will be published to confirm the completion of Staff's review and to outline the intended implementation date of the changes.

CBOE CANADA INC.

PROPOSED PUBLIC INTEREST RULE AMENDMENT

DIRECTED INDICATIONS OF INTEREST

REQUEST FOR COMMENTS

Introduction

In accordance with Schedule 4 to its recognition order, Cboe Canada Inc. ("Cboe Canada" or the "Exchange") is publishing a proposed public interest rule amendment (the "Public Interest Rule Amendment") to its trading rules (the "Trading Policies") to add a new order type to the Exchange's MATCHNow Trading Book: the Directed Indication of Interest (the "Directed IOI").{1} The Public Interest Rule Amendment was filed with the Ontario Securities Commission (the "OSC") and is being published for comment. A description of the Public Interest Rule Amendment is set out below, and the text of the Public Interest Rule Amendment is set out in Appendix A. Subject to (a) any changes resulting from the comments received, (b) the approval of the OSC as contemplated in section 10(f) of Schedule 4 of the Exchange's recognition order, and (c) the granting of an order for exemptive relief on the basis of the application being filed by the Exchange in connection with the publication of this notice (as explained in greater detail below in the section entitled "Exemptive Relief from 'Pre-Trade Transparency' Requirement"), the Public Interest Rule Amendment will be effective on a date to be confirmed subsequent to the publication of the notice of approval and the exemptive relief order on the OSC's website.

Description of the Public Interest Rule Amendment

The Exchange is proposing to offer a new order type, the Directed IOI, by adding a new Section 9.09 (Directed IOIs), under Part IX (Trading in MATCHNow) of the Trading Policies and making one consequential amendment to Section 9.02 of the Trading Policies (to add "Directed IOI" as a new order type available on MATCHNow).

As proposed, Directed IOIs will allow a Member to use Cboe BIDS Canada to invite, on a conditional basis, one or more of its Sponsored Users to firm up an offer to buy or sell any security currently available for trading on MATCHNow, but only if each such Sponsored User has previously (confidentially) expressed an interest in buying or selling a large block-sized position in that security and enabled the Directed IOI feature for that position via "BIDS Trader" (the Cboe BIDS Canada desktop interface for Sponsored Users, which is fully integrated with each Sponsored User's order management system or "OMS"{2}). In this sense, Directed IOIs will be similar to Conditionals, but distinctive. Further details are provided below.

Overview of Directed IOI Functionality

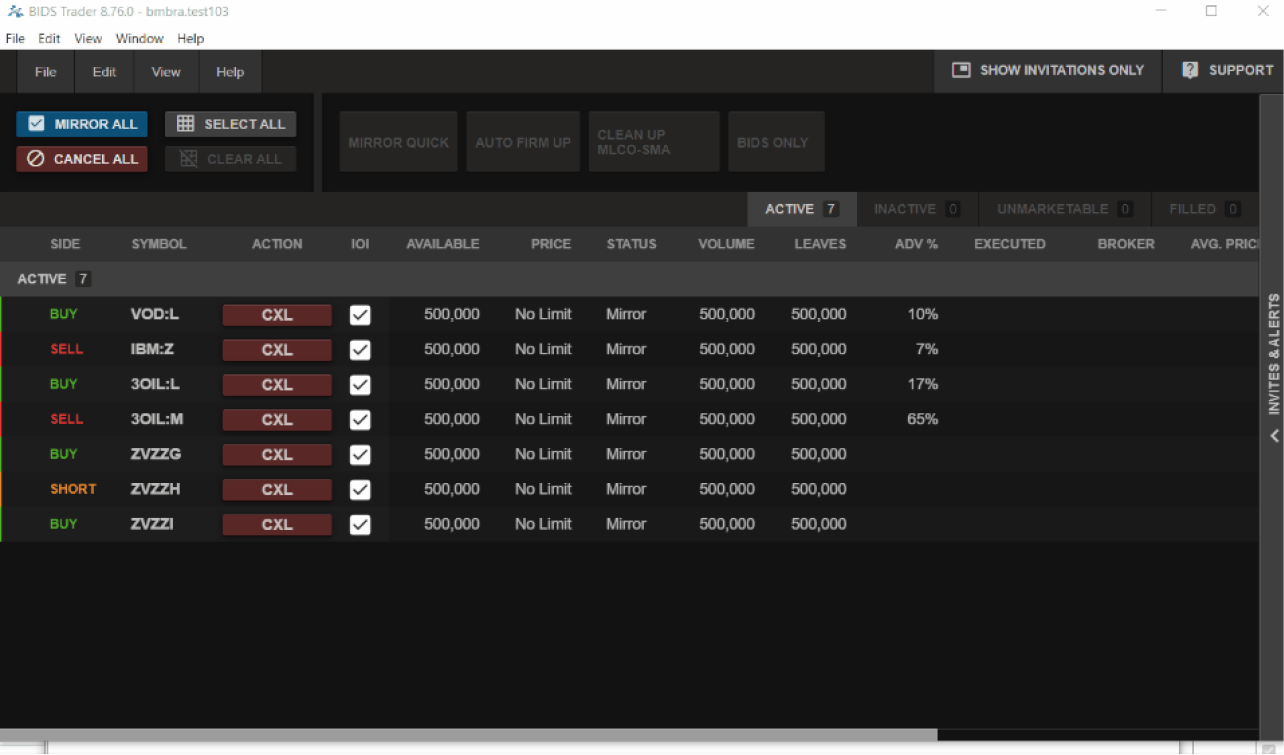

A Directed IOI can only be originated by a Member. The Directed IOI will consist of a message transmitted by the Member to Cboe BIDS Canada, which the system will then transmit to the Sponsored User client(s) that the Member has selected; however, the message will only be transmitted (displayed) to a selected Sponsored User if (a) there is sufficient uncommitted liquidity in the Sponsored User's OMS and (b) the Sponsored User has checked the "IOI" box on BIDS Trader for that uncommitted liquidity. (See Screenshot 1.)

Screenshot 1

The Member will not know in advance of sending a Directed IOI which (if any) of its Sponsored User clients meet the criteria, nor will it receive any kind of confirmation that a selected Sponsored User does not meet the criteria after the Directed IOI has been sent.

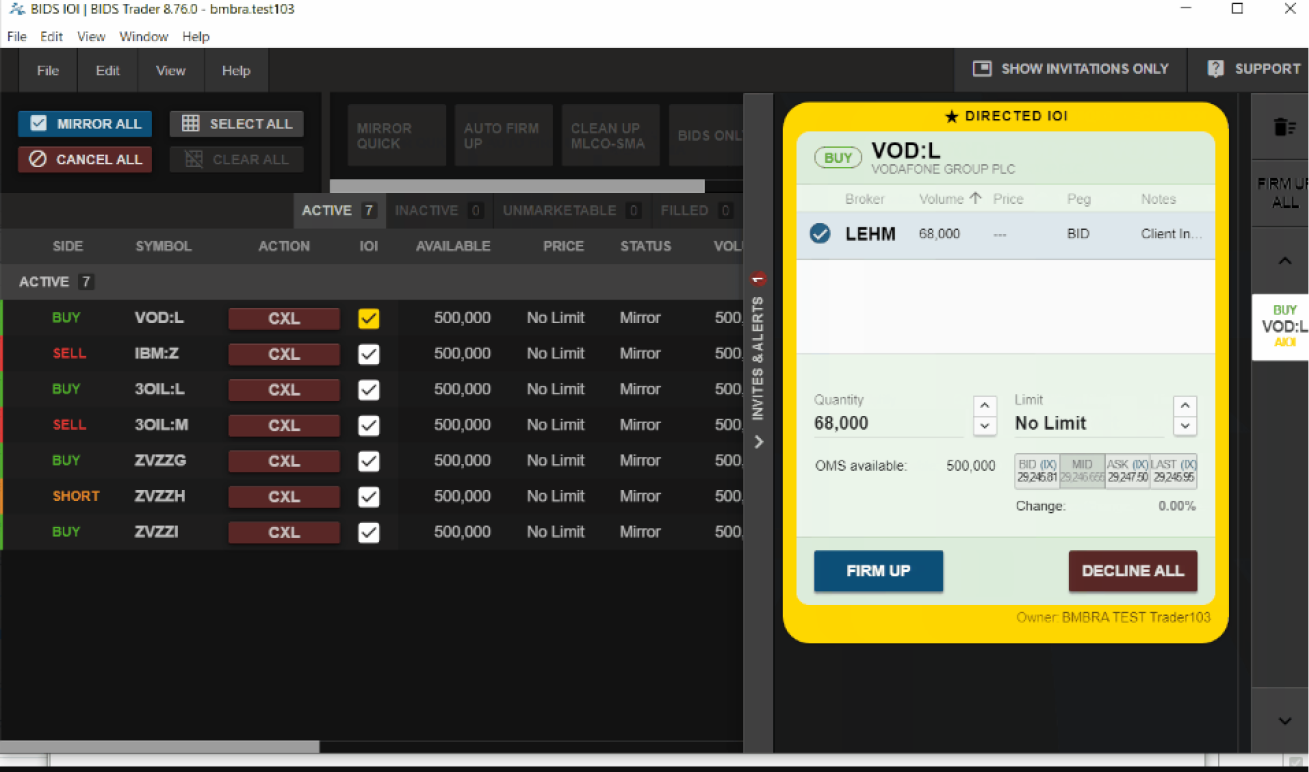

When a Directed IOI is received by a Sponsored User, a pop-up will occur and the "IOI" box on BIDS Trader will turn yellow. (See Screenshot 2.) This is a visual cue to the Sponsored User that the position is tradeable and available for firm-up, even after the pop-up disappears (which it does after 30 seconds).

Screenshot 2

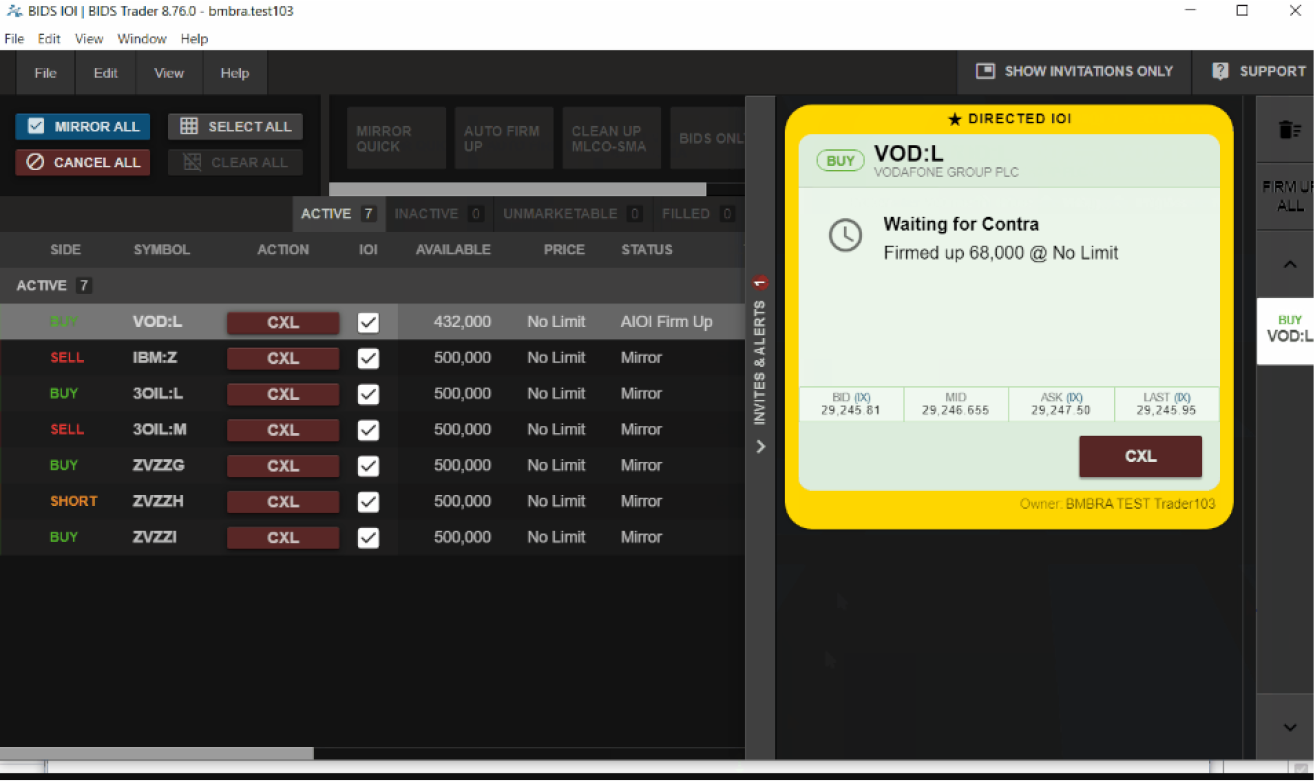

If the Sponsored User firms up the invitation (by clicking the blue "FIRM UP" button in the pop-up), the message inside the pop-up switches to "Waiting for Contra" (see Screenshot 3 below), at which point the originating Member becomes the sponsoring dealer on the resulting (buy-side) order. Note that, as part of its firm-up message, the Sponsored User may either maintain the default values for quantity and limit price that the system has generated based on instructions or settings previously input by the Sponsored User, or it may enter a new value for quantity and/or limit price, so long as the new value(s) does (do) not make the order too small to meet the applicable minimum size threshold (see the section entitled "Minimum Size Threshold" under the heading "Rationale and Relevant Supporting Analysis" below), nor too large to be satisfied by the uncommitted liquidity that is available in the Sponsored User's OMS at that moment.

Screenshot 3

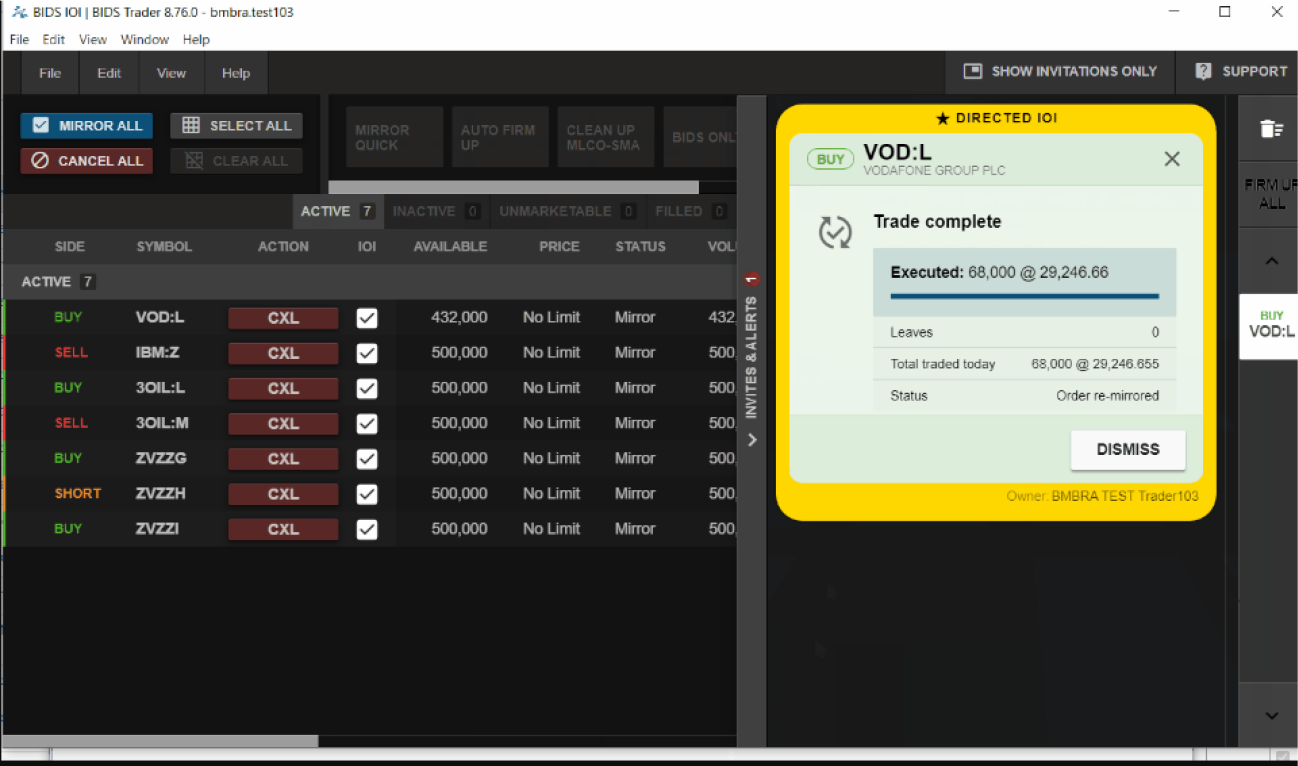

For the process to continue, the originating Member must then take the affirmative step of firming up, at which point the trade is immediately executed. The Sponsored User also immediately receives a final pop-up confirming the execution of the trade (see Screenshot 4), and the orders and trade are simultaneously printed to the public tape on Cboe Canada (via the MATCHNow Trading Book).

Screenshot 4

In the event the Member does not firm up, the Directed IOI is cancelled and no trade occurs.

Information/Flow Restrictions

1. From the Member's perspective

After sending a Directed IOI, the Member does not receive a notification (or any other information) unless and until the recipient Sponsored User (or one of the recipient Sponsored Users) has firmed up. If more than one Sponsored User was selected to receive the Directed IOI, the Member only receives a single notification-namely, upon firm-up by the first Sponsored User to act; conversely, if none of the selected Sponsored Users firms up, the Member receives no notification.

2. From the Sponsored User's perspective

BIDS Trader allows a Sponsored User to narrow the type of liquidity that it receives via Directed IOI. The criteria that a Sponsored User can activate to narrow the Directed IOI messages it receives are the following{3}:

Members select the appropriate criteria when sending a Directed IOI so that the message accurately reflects the underlying liquidity; if no criteria are selected, the system defaults to the most permissive options (e.g., "Potential").{4} On the Sponsored User side, the system will filter out messages that do not meet the criteria selected by the Sponsored User. In those cases, the Sponsored User does not glean any additional information, but rather, it simply does not receive any messages (information) at all, as it will not be made aware of any Directed IOIs that do not meet its needs.

Price

Directed IOIs can only be executed at or within the range of prices established by the protected National Best Bid or Offer (the "NBBO"), subject to a peg (if that feature is activated by the Member and/or the Sponsored User).

Time Constraints

For a Sponsored User, there is no time constraint applicable to the firm-up; instead, the system allows the Sponsored User to firm up for as long as the Directed IOI remains active. However, the longer a Sponsored User waits to firm up, the greater the risk that the indicated liquidity will disappear, either because another Sponsored User has acted upon it or because the Member has cancelled the Directed IOI altogether (which it can do at any time prior to a Sponsored User's firm-up). In either case, the yellow indication disappears for the position on the Sponsored User's BIDS Trader screen (and, if applicable, the pop-up on the screen grays out).

As for the Member, once its Directed IOI has been firmed up by a Sponsored User, the system imposes a time limit of one second on the Member to firm up, after which the firmed-up message from the Sponsored User is cancelled; this is similar to the time constraint that applies to a Member when receiving a firm-up message for a Conditional on Cboe BIDS Canada under existing Exchange Requirements.{5}

Sequencing

The system allows multiple Sponsored Users to receive a single Directed IOI invitation from a Member simultaneously; however, as soon as one of the Sponsored Users firms up, the invitation is automatically cancelled for the other Sponsored User(s).

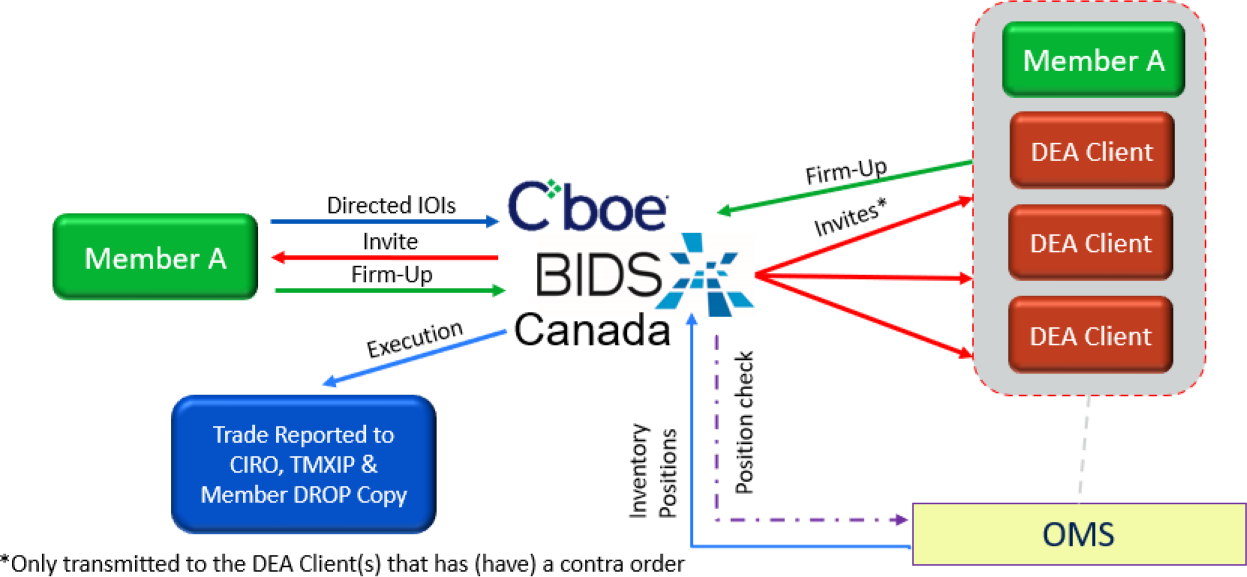

The following graphic illustrates the workflow process:

- Member A sends a Directed IOI for symbol XYZ via Cboe BIDS Canada to several of its DEA Clients that have been onboarded to receive them.

- Cboe BIDS Canada detects potential (uncommitted) liquidity in the OMS for three of the DEA Clients that have been selected by the Member and transmits the message to them simultaneously.

- One of the DEA Clients firms up via the BIDS Trader desktop interface (which prevents any other DEA Client from firming up thereafter).

- The firmed-up invitation message is sent back through Cboe BIDS Canada to Member A.

- Member A firms up, and the trade is immediately executed and reported.

The Exchange believes that the specificity of the criteria and the robustness of the processes that will govern the entry, execution, and regulatory reporting of Directed IOIs on Cboe BIDS Canada are precisely the type of factors that the Canadian Securities Administrators (the CSA) have implicitly acknowledged as relevant and important in deciding whether or not to permit the use of IOIs in a dark pool context. See CSA/IIROC Joint Staff Notice 23-308, Update on Forum to Discuss CSA/IIROC Joint Consultation Paper 23-404 "Dark Pools, Dark Orders and Other Developments in Market Structure in Canada" and Next Steps (2010) 33 OSCB 4747 at 4748 (May 28) (the "2010 Joint Notice") (available at https://www.osc.ca/sites/default/files/pdfs/irps/csa_20100528_23-308_update-dark-pools.pdf) (noting that the "main issues related to IOIs disseminated by dark pools in order to attract order flow" could potentially be addressed through "enhanced transparency of marketplaces' practices regarding the dissemination of information respecting orders and trades, including the provision of IOIs").{6}

Other Implementation Details

The Exchange already has an outsourcing agreement in place with its affiliate with respect to the technology that will support the new proposed functionality, and that agreement contains broad language concerning the technology licensing and support services to be provided by that affiliate to the Exchange; as such, that agreement will not require any amendments. In a similar vein, Directed IOIs fit within the term "instructions" and/or the term "messages" referred to in the context of Cboe BIDS Canada set out in existing language in subsections 6(f) and 6(g) of the Cboe Canada Member Agreement (available at https://www.cboe.ca/documents/en/trading-data/cboe-canada-member-agreement-20240331-en.pdf), which language, among other things, describes the obligations under applicable Exchange Requirements of a Sponsoring Member that uses Cboe BIDS Canada; as such, no amendments to the Member Agreement will be necessary.

With regard to onboarding, the Exchange will continue to rely on the licensed systems and support services provided by its affiliate, which provide a reasonable assurance that each institutional investor that wishes to receive Directed IOIs has and maintains the necessary relationship with the relevant Sponsoring Member(s) before it can be onboarded for Directed IOIs. Moreover, as is the case for any Cboe BIDS Canada-based activity, the system will prevent any Directed IOIs from being transmitted to a Sponsored User unless and until the appropriate risk controls have been established for that Sponsored User by the relevant Sponsoring Member(s).

Expected Date of Implementation

The Exchange is seeking to implement this Public Interest Rule Amendment in Q1 of 2025.

Rationale and Relevant Supporting Analysis

Directed IOIs Offer Benefits Over Traditional Indications of Interest

Indications of interest ("IOIs") have been used for decades by marketplace participants in Canada-and in financial markets around the world-as a tool for finding and trading large block-sized liquidity. One scenario in which IOIs may be used is where a securities dealer is "working" a large order for a listed security-i.e., searching for a counterparty for a large client or proprietary order in a manner that minimizes the risk of a significant price swing due to the volume of the order; where a match is found and agreed to orally or in writing, the resulting trade must then be entered for execution on a marketplace, pursuant to subsection 6.4(1) of the Canadian Investment Regulatory Organization's ("CIRO") Universal Market Integrity Rules ("UMIR"). At that point, it is immediately reported by the marketplace on which it was entered to an information processor, pursuant to section 7.2 of National Instrument 21-101 Marketplace Operation ("NI 21-101"); it is also reported (along with all mandatory "audit trail" designations and other data) to CIRO.{7} This type of activity has traditionally been referred to as the "upstairs market"; and where it involves a single securities dealer acting on both sides of the trade, it can be seen as a form of "internalization." As observed by the CSA and CIRO in a joint notice published in 2019:

[I]nternalization can refer to different types of trading activities, and may occur through a variety of means. One method is [...] where a dealer may work to find the counterparty to a client order or commit its capital and assume the risk of acting as the trade counterparty on a principal basis. Commonly referred to as the "upstairs market", withholding larger orders from immediate entry to a marketplace is a long-standing practice in the Canadian market.

Joint CSA/IIROC Consultation Paper 23-406, Internalization within the Canadian Equity Market (Mar. 12, 2019), s. 5.1 (available at https://www.osc.ca/sites/default/files/pdfs/irps/csa_20190312_internalization-within-the-canadian-equity-market.pdf) (the "2019 Consultation Paper").

Over the years, traditional IOIs went from being negotiated in person or by telephone, to being transmitted by message boards and other electronic communication methods. And as noted by the CSA and CIRO, the execution of large block-sized orders that originate as IOIs has a beneficial impact on Canadian securities markets. See ibid. ("[W]e believe such ["upstairs market'] activities to be potentially integral to both the execution of large investor orders and efficient functioning of the Canadian market.").

However, the traditional methods used by market participants to communicate IOIs involve many disadvantages, including, in particular:

- Risk of information leakage: In many cases, IOI messages posted to public or semi-public platforms can be accessed by parties who have no bona fide interest in trading. This allows such parties to take advantage of the information to inform their trading strategy, without any downside or other form of accountability.

- Unreliability: Traditional IOIs can quickly become stale without the recipients' knowledge, leading to inefficiencies where recipients attempt to initiate a negotiation process based on an outdated IOI message.

- Market volatility: Traditional IOIs, due to their widespread availability, can cause market participants to take a defensive posture, fearing a potentially large movement in price as a result of the potentially large order that may lie behind the IOI, thereby setting off a chain reaction of trades that result in a self-fulfilling prophecy of significant price swings.

- Lack of standardized regulatory reporting: Depending on how an IOI is negotiated and executed, the manner of reporting the resulting trade is not standard or systematic across dealers, especially in cases where the IOI is executed off-exchange (in circumstances or jurisdictions where that is permitted). See, e.g., Cboe Global Markets, Inc., "Off-Exchange Trends: Beyond Sub-dollar Trading" (May 17, 2023) (available at https://www.cboe.com/insights/posts/off-exchange-trends-beyond-sub-dollar-trading/) ("[N]on-ATS OTC venues are bilateral, including venues such as single dealer platforms, wholesalers, central risk books and traditional high touch broker crossing/capital commitment. [...] [T]hese venues do not have regulatory filing requirements specific to their operations. Increased transparency into the types of venues represented off-exchange could create a fairer competitive landscape [...].").

Directed IOIs represent an automated process that offers a more efficient and reliable alternative to traditional IOIs.>{8}They are particularly useful to securities dealers (or "sell-side" firms) that operate Central Risk Books, but they also respond to the needs of large institutional investor firms (or "buy-side" firms), as they provide an integrated workflow solution for sourcing block-sized liquidity, specifically designed to address many of the disadvantages of traditional IOIs, including:

- Information restrictions: Directed IOIs ensure that invitations are targeted only to buy-side firms that have uncommitted liquidity in a specific security, with the necessary volume. In this way, information about the contra side is only sent to those parties that are objectively and demonstrably interested in potentially executing block-sized orders, thereby reducing the risk of any undue advantage for either side, while also reasonably ensuring that the receiving (buy-side) parties are not overwhelmed with invitations, as they only receive messages that are appropriate to them, based on their needs at any given moment of the trading day.

- Reliable, up-to-date messaging: The system ensures that Directed IOI messages are kept up to date at all stages of the matching process, with accurate sizing and pricing or automatic cancellation where the liquidity is no longer available.

- Less price volatility: Directed IOIs are sent exclusively to Sponsored Users that have an interest in trading the security in question. Even if the Member chooses a specific Sponsored User client as a recipient of a particular Directed IOI, that Sponsored User will not become aware of the invitation if there is no (or an insufficient volume of) uncommitted liquidity for that security in the Sponsored User's OMS, or if the Sponsored User's limit price is too restrictive. In this way, the risk of defensive trading by a large number of market participants-and the undue price fluctuations that follow-is reduced.

- Greater efficiencies: Directed IOIs keep the entire trade lifecycle electronic and traceable and allow for IOIs to be identified and reported more accurately as part of the electronic data recorded by the system.

In addition, Directed IOIs will leverage existing Cboe BIDS Canada infrastructure and will make the platform consistent with equivalent BIDS-powered platforms operated by Cboe Canada affiliates in other regions of the world, ensuring that Canadian buy-side firms have access to the same standard services as offered to buy-side firms in those other regions.

Minimum Size Threshold

Consistent with the goal of providing an automated solution for sourcing block-sized liquidity and for conducting "upstairs market" negotiations, Directed IOIs will be subject to a minimum notional threshold of $100,000 in value.

Balancing Pre-Trade Transparency and the Need to Contain Information Leakage

When it comes to large block-sized orders, some degree of pre-selection between counterparties is appropriate and necessary, as it prevents the information leakage and resulting market distortions that can arise if such orders are required to be routed to fully transparent marketplaces that effectively allow all marketplace participants to see the liquidity underlying such orders. As the OSC stated in its June 2017 approval notice for Liquidnet Canada Inc. ("Liquidnet") with regard to a feature that is functionally similar to Directed IOIs (known as "targeted invitations"):

[F]air access and pre-trade transparency are critical to an efficient and effective market. However, we also see the value in facilitating large executions for buy-side investors without providing their order details to the broader market or increasing their market impact costs.

In re Liquidnet Canada Inc. -- Changes to Form 21-101F2 -- Notice of Commission Approval, (2017), 40 OSCB 5114 (June 8) (available at https://www.osc.ca/sites/default/files/2020-12/306.pdf) ("2017 Liquidnet Approval").

As noted above, Directed IOIs will be subject to a considerable minimum size threshold ($100,000 in notional value). This exceeds the standard minimum size threshold of 50 standard trading units and $30,000 or $100,000 applicable under UMIR 6.6 (which allows a dark order to execute without providing price improvement), thus enabling Directed IOIs to strike an appropriate balance between the competing policy goals of promoting price discovery (through mandatory pre-trade price transparency) and preventing the costly and harmful effects of information leakage and undue price volatility. See, e.g., 2019 Consultation Paper, supra, s. 4.1 ("Some client orders may be of sufficient size that they would trade through multiple price levels in an order book resulting in 'market impact' and a less advantageous execution outcome."); see also 2009 Consultation Paper, s. IV(iv) ("The concerns raised by the practice of Dark Pools sending IOIs can be countered by the potential benefit that these communications can bring including greater success in the search for liquidity. [...] Increased likelihood of information leakage and gaming can be offset by the ability to facilitate finding liquidity quickly and improving the execution obtained by the user, an ability which could become more important as the number of Dark Pools increase."). This beneficial effect on price stability is in line with one of the primary purposes that dark pools served when they first emerged more than two decades ago. See ibid. s. IV(ii) ("[T]he first Dark Pools originally facilitated the execution of large block trades that would significantly impact the market if traded on a visible marketplace.").{9}

In short, Directed IOIs represent a simple and systematic way to automate the long-standing practice of working up large block trades through the "upstairs market," which-as noted above-the CSA and CIRO have acknowledged as "potentially integral" to the efficient functioning of capital markets in Canada. See 2019 Consultation Paper, supra, s. 5.1.

Expected Impact on Market Structure, Members, Investors, Issuers and Capital markets

The impact on market structure, Members, investors, and capital markets is expected to be positive, through the resulting expansion of liquidity and increased matching and price improvement opportunities for large-sized orders. Cboe Canada anticipates further electronification of the block market in Canada, which presently represents approximately 5% to 10% of overall volume. Furthermore, Cboe Canada does not expect Directed IOIs to divert order flow away from protected transparent markets, nor does Cboe Canada expect any material cannibalization of existing Conditional order flow on the MATCHNow Trading Book. Rather, Cboe Canada expects Directed IOIs to provide an efficient alternative for traders dealing with large orders through more traditional IOI channels and/or competing service offerings by other dark marketplaces.

Expected Impact on Exchange's Compliance with Ontario Securities Law and on Requirements for Fair Access and Maintenance of Fair and Orderly Markets

The proposed change will have no impact on Cboe Canada's continuing compliance with Ontario securities law, including requirements for fair access and the maintenance of fair and orderly markets for the reasons outlined immediately below.

1. No Restriction of "Fair Access"

Cboe Canada submits that Directed IOIs are fully compliant with "fair access" requirements under section 5.1 of NI 21-101. As a tool specifically designed to facilitate and automate block-sized orders, Directed IOIs are based on "reasonable standards for access" and do not "unreasonably create barriers to access to the services provided by the marketplace." 21-101CP, s. 7.1(1). In addition, the new feature is expected to further incentivize onboarding of market participants to Cboe BIDS Canada, both on the sell side and the buy side, thereby providing more matching opportunities for large orders, often with price improvement, without any significant market distortions or erosion of price discovery. This represents a net benefit to the Canadian capital markets as a whole.

2. Directed IOIs Comply with "Order Protection" Requirements

Section 6.1 of National Instrument 23-101 Trading Rules imposes an "order protection" requirement on all marketplaces, i.e., an obligation to adopt policies and procedures that are reasonably designed to prevent trade-throughs (unless the trade-through is expressly permitted by section 6.2). Because Directed IOIs can only be executed at or within the NBBO (as noted above), the feature effectively prevents trade-throughs.

3. Directed IOIs Mitigate Information Leakage

As explained under the heading "Directed IOIs Offer Benefits Over Traditional Indications of Interest" in the "Rationale and Relevant Supporting Analysis" section above, Directed IOIs offer several advantages over traditional IOIs-and, in particular, with regard to information leakage. As noted above, Directed IOIs narrow the pool of recipients of a dealer's (Member's) indications to eligible large institutional investor clients (Sponsored Users) that have relevant contra-side uncommitted liquidity; Sponsored Users that have no (or insufficient) uncommitted liquidity for the relevant security will not be notified of the Member's willingness to trade that security. Conversely, Members will not have any advance knowledge of which, if any, of their Sponsored User clients are prepared to trade, nor will they be notified whether or not any of their selected Sponsored User clients have actually received a Directed IOI; a Member is only notified of contra-side interest if and when one of its selected Sponsored User clients firms up.

In addition, by automating the various steps in the process and providing Sponsored Users with a consolidated view of their Directed IOI activity via a desktop interface, Sponsored Users can easily monitor the frequency with which their Sponsoring Members are actually executing Directed IOI-originated trades. Thus, the system incentivizes higher firm-up rates by Members than would otherwise occur, since Sponsored Users, over time, will tend to favour Members that firm up more consistently. This further mitigates the risk of information leakage.

Ultimately, we respectfully submit that interpreting Canadian securities regulations in a manner that would effectively prohibit a marketplace from offering a service that simply automates and increases the efficiency of a long-standing dealer practice seems unwarranted; furthermore, it creates a significant risk that Canadian marketplace participants will be at a disadvantage as compared to their international counterparts, to the extent that the equivalent of Directed IOIs is already available in jurisdictions outside of Canada. (See the section under the heading "New Feature or Rule" below for details regarding direct equivalents to Directed IOIs currently in use in other jurisdictions.)

4. Exemptive Relief from "Pre-Trade Transparency" Requirement

Directed IOIs may involve the "display" of order information by the Member to the Sponsored User and vice-versa. As a "dark" order book, however, MATCHNow does not immediately transmit orders to an information processor, as is required of marketplaces that display orders, pursuant to subsection 7.1(1) of NI 21-101. {10}As such, under separate cover, Cboe Canada has submitted an application by "coordinated review" of the OSC and the other 12 jurisdictions of the CSA for exemptive relief under section 15.1 of NI 21-101 for Directed IOIs from the pre-trade transparency requirements of subsection 7.1(1) of NI 21-101. The new Directed IOI feature will not be implemented until such time as the exemptive relief has been granted, or it has been determined in consultation with OSC staff that such relief is not required.

Consultation and Internal Governance Process

Cboe Canada has conducted informal one-on-one consultations with several Members representing different firm sizes and business models, including large bank-owned dealers that operate Central Risk Books; Cboe Canada has also conducted meetings with numerous buy-side firms (including existing Sponsored Users and some buy-side firms that may become Sponsored Users).{11} The feedback received from those informal consultations and meetings was overwhelmingly positive. In addition, the proposed change was discussed and approved by the Executive Committee and by the Regulatory Oversight Committee of the Exchange's board of directors.

Certain Information Specific to a Proposed Fee Change

Not applicable.

Expected Impact on the Systems of Members or Service Vendors

Making use of Directed IOIs is voluntary. For Members and Sponsored Users that elect to make use of Directed IOIs (and the vendors who service those Members and Sponsored Users), any impact on their systems will be minimal, as the proposed change will simply require creating the ability to enter a value for the new FIX Tags that Cboe Canada will establish for the new feature. Cboe Canada believes that a reasonable estimate of the time needed for Members, Sponsored Users, and service vendors to modify their own systems in this way is 60 days or less, based on previous experiences with the creation of new FIX Tags.

Rationale for Why the Proposed Significant Change Is Not Considered a Significant Change Subject to Public Comment

Not applicable.

Alternatives Considered

No alternatives were considered.

New Feature or Rule

For several years now, Liquidnet and its affiliates around the globe have offered a trading functionality for equity securities known as "Targeted Invitations," which are similar (albeit not identical) to Directed IOIs.{12} The Liquidnet proposal was published for comment in November 2016 (see https://www.osc.ca/en/industry/market-regulation/marketplaces/alternative-trading-systems-atss/atss-operating-ontario/liquidnet-canada-orders-notices/notice-proposed), along with an OSC Staff notice (see https://www.osc.ca/sites/default/files/2021-01/761.pdf). The OSC granted approval for the feature in June 2017 (see 2017 Liquidnet Approval, supra), along with certain related exemptive relief (see In re Liquidnet Canada, Inc. (June 6, 2017), available at https://www.osc.ca/en/securities-law/orders-rulings-decisions/liquidnet-canada-inc-s-151-ni-21-101-marketplace-operation).{13}The feature continues to be in use today.

In addition, several Cboe Canada affiliates already offer the equivalent of Directed IOIs to sell-side and buy-side firms in the jurisdictions where these marketplaces are regulated-specifically, the United States (in the case of BIDS Trading L.P.), the United Kingdom (in the case of Cboe Europe Limited), and the Netherlands (in the case of Cboe Europe B.V.). See BIDS Form ATS-N, supra, Part III, Item 7 (describing "conditional AIOIs"); see also Cboe Europe Equities, Cboe BIDS Europe Service Description, s. 5 (entitled "Directed IOIs") (available at https://cdn.cboe.com/resources/participant_resources/CboeEuro_BIDS_Service_Description.pdf).{14}

Comments

Comments should be provided, in writing, no later than November 25, 2024, to:

Joacim WiklanderChief Executive Officer and PresidentCboe Canada Inc.65 Queen Street WestSuite 1900Toronto, ON M5H 2M5

with a copy to:

Trading & Markets DivisionOntario Securities Commission20 Queen Street West20th FloorToronto, ON M5H 3S8

Please note that, unless confidentiality is requested, all comments will be publicly available.

APPENDIX A

BLACKLINE OF CBOE CANADA TRADING POLICIES REFLECTING PUBLIC INTEREST RULE AMENDMENT

9.02 Additional Orders and Modifiers Available in MATCHNow

| Conditionals | A conditional order or message which, if firmed up, becomes an order that may execute during the Continuous Trading Session in MATCHNow against other firmed-up Conditionals or opted-in Market Flow Orders or Liquidity Providing Orders. |

| Directed Indication of Interest ("Directed IOI") | A conditional indication of interest sent by a Member to one or more of its Sponsored Users via Cboe BIDS Canada. |

[...]

9.09 Directed IOIs

(1) A Directed IOI may be initiated by any Member that has been onboarded to do so through Cboe BIDS Canada.

(2) The Member shall designate, in the manner indicated by the Exchange, one or more Sponsored Users as potential recipients of its Directed IOIs. Sponsored Users may not be designated to become recipients of Directed IOIs until such time as all relevant risk controls and other appropriate onboarding-related tasks have been completed in accordance with the relevant Exchange Requirements.

(3) Each Directed IOI entered by a Member must have a notional value greater than $100,000.

(4) At the moment of entry of a Directed IOI, the Member shall select one or more of its designated Sponsored Users as recipient(s) of the Directed IOI.

(5) Only Sponsored Users that (a) have uncommitted liquidity sufficient to fulfill the potential order represented by the Directed IOI and (b) have made an affirmative selection for that uncommitted liquidity via the Cboe BIDS Canada interface shall receive a notification for the Directed IOI.

(6) The Sponsored User(s) must firm up the Directed IOI for the matching process to proceed; if no firm-up occurs, the Directed IOI will remain on Cboe BIDS Canada until it is cancelled, which occurs either at the time of expiration chosen by the Member or at the end of the trading day, whichever is earlier.

(7) If the Sponsored User firms up-or, in the case of multiple Sponsored Users, at the moment when the first Sponsored User firms up-a message is sent back to the Member, which has the option to firm up within one second. If it does so, the trade is executed; if it does not firm up within the one-second time limit, no trade occurs and the Directed IOI is cancelled.

(8) The execution price of a Directed IOI shall be at or within the NBBO, subject to any peg selected by the Member and/or the Sponsored User.

[1] Capitalized terms used but not defined herein are as defined in the Trading Policies.

[2] BIDS Trader is not used by Members; it is a graphical user interface (or "GUI") that only runs on the desktops of Sponsored Users.

[3] These criteria are consistent with the "Framework" set out in the Asia Pacific Equities IOI Charter issued in November 2020 (the "Charter") as a joint project of the Asia Securities Industry & Financial Markets Association and various other industry organizations. For additional details, please see https://www.asifma.org/wp-content/uploads/2020/11/asia-pacific-equities-ioi-charter-2020.11.19-vf.pdf; see also https://www.asifma.org/resource/asia-pacific-ioi-charter/ (noting that the Charter "uses the internationally recognised standard created in the 2017 [Association for Financial Markets in Europe/The Investment Association or 'AFME/IA"] Framework and provides additional clarification on certain AFME/IA subclasses and behaviours, with the intention of improving the transparency and consistency of approach across participants" and "takes into account the [...] the 2018 and 2019 Circulars released by the Hong Kong Securities and Futures Commission around the implementation of IOIs").

[4]It is anticipated that the system will be designed to require a positive value in the FIX Tag that identifies the liquidity source before a Member's initial Directed IOI message will be permitted to be transmitted to Cboe BIDS Canada, even if it is simply the "default" value; this will reasonably ensure accountability for Members, in terms of how they are identifying the liquidity source for their Directed IOIs and whether they are doing so appropriately.

[5]See the "Commentary" under existing Section 9.08(1) of the Trading Policies. Note that, on Cboe BIDS Canada, Sponsored Users must act through human traders, whereas Members must act through algorithmic (automated) trading systems. This important distinction explains why the two types of traders are not subject to an identical time constraint.

[6] In summarizing the public comment letters that were received in response to a request for comment published in 2009 (see Joint Canadian Securities Administrators/Investment Industry Regulatory Organization of Canada Consultation Paper 23-404, Dark Pools, Dark Orders, and Other Developments in Market Structure in Canada (Sept. 3, 2009) (the "2009 Consultation Paper") (available at https://www.bcsc.bc.ca/-/media/PWS/Resources/Securities_Law/Policies/Policy2/Consultation-Paper-23404.pdf?dt=20200325221305)), the 2010 Joint Notice observed that there were "mixed" views on whether or not dark pools "should be permitted to select which destinations are able to receive IOIs"; however, the CSA acknowledged that some commenters were of the view that "it should be the subscribers of the Dark Pools that have the ability to select the destination for their IOIs, based on their clients' interest," and that a "few" other commenters thought it "important that dark pools have the flexibility to target recipients of communications and that this could be based on commercial relationships, business goals and needs, technology and probability of execution." 2010 Joint Notice at 4752-53.

[7] An IOI, in and of itself, is not reportable to CIRO unless and until it is "actionable" or "firm," at which point it becomes an "order" for the purposes of section 1.1 of NI 21-101, and that makes it reportable to CIRO pursuant to UMIR 10.11(2), even if it is not executed. (In practice, the marketplace that received and, if applicable, executed the order transmits the order to CIRO, via the Market Regulation Feed, in accordance with the standard terms of a regulation services agreement with CIRO.) For a more detailed discussion of this issue, please see the discussion below under the heading "A Directed IOI Only Becomes an Order Upon Firm-Up."

[8] There has been some debate about whether a technology that automates the internalization of orders should be understood as a function inherent to a marketplace or one that is inherent to a dealer, but the "marketplace" approach does appear to be the prevailing view. See, e.g., Joint CSA/IIROC Staff Notice 23-327, Update on Internalization within the Canadian Equity Market (2020), 43 OSCB 6504 (Aug. 20) (available at https://www.osc.ca/sites/default/files/2020-11/csa_20200820_23-327_csa-iiroc-internalization-canadian-equity-market.pdf) (the "2020 CSA Notice"), s. II(A)(iv) ("Most commenters were of the view that systems that automate the internalization of orders should be considered a marketplace, and that relevant provisions of the rules should apply."). It is our view that the Directed IOI functionality as proposed does not cause Cboe Canada to replace its Members, each of which must be a registered dealer, but rather, it merely allows the Exchange to support those registered dealers in carrying out an activity that they have been doing for decades (locating block liquidity through IOIs) in a more efficient and effective manner. So, when it comes to Directed IOIs, both the dealer and the marketplace have their respective roles to play. To put it another way, the Directed IOI activity that would be conducted by the dealers (Sponsoring Members) through the proposed Cboe Canada functionality would not transform Cboe Canada into a dealer, any more so than any other trading activity would; each dealer (Sponsoring Member) will remain responsible for each Directed IOI that results in a firm order on behalf of itself and its DEA Client (Sponsored User), just as a dealer is responsible for any DEA-based trade that it originates or supports, and the marketplace (Cboe Canada) will be responsible for facilitating the bringing together of (potential) orders and the matching that occurs when the Directed IOI is firmed up by both parties. As such, the functionality does not raise any new registration requirements.

[9] Although never adopted, a similar large threshold-based approach was considered in the United States. Specifically, in 2009, the U.S. Securities and Exchange Commission (the "SEC") proposed rule amendments that would have exempted actionable IOIs valued at $200,000 or higher from pre-trade transparency requirements that otherwise would have become expressly applicable to them under the proposed rules. See Securities Exchange Act Release No. 60997 at (Nov. 13, 2009) (available at https://www.sec.gov/rules/proposed/2009/34-60997.pdf). As stated in the release, the SEC recognized "the need for targeted size discovery mechanisms that can enable investors to trade more efficiently in sizes much larger than the average size of trades in the public markets" and, therefore, it was proposing to exclude from the proposed new definitions of "bid" and "offer" any actionable IOIs "for a quantity of NMS stock having a market value of at least $200,000" that were "communicated only to those who are reasonably believed to represent current contra-side trading interest of at least $200,000". Ibid. See also Paul G. Mahoney, co-author. "The Regulation of Trading Markets: A Survey and Evaluation." Gabriel Rauterberg, co-author. In Securities Market Issues for the 21st Century, edited by Merritt B. Fox et al., 221-81 at 243. New Special Study of the Securities Markets. New York: Columbia Law School, 2018. (available at https://repository.law.umich.edu/cgi/viewcontent.cgi?article=1121&context=book_chapters) (confirming that the amendments proposed in 2009 had not been adopted).

[10] See, e.g., CSA Consultation Paper 21-403 -- Access to Real-Time Market Data, (2022), 45 OSCB 9488 at 9492 (Nov. 10) (available at https://www.osc.ca/sites/default/files/2022-11/csa_20221110_21-403_real-time-market-data.pdf) ("Pursuant to the transparency requirements set out in Part 7 of NI 21-101, transparent marketplaces must provide to the equity IP all orders and trades, whereas dark marketplaces must provide only trades.").

[11]Pursuant to an amalgamation that became effective on January 1, 2024 (the "Amalgamation"), the operations of the alternative trading system ("ATS") operated by the then TriAct Canada Marketplace LP ("TriAct"), were absorbed into the Exchange as a new Trading Book. For meetings that occurred prior to January 1, 2024, the meetings were in fact conducted by personnel acting on behalf of the then-TriAct, and the sell-side dealer firms that were consulted were technically "Subscribers" of the ATS operated by TriAct at the relevant time (as opposed to "Members" of the Exchange).

[12] For details on how Targeted Invitations function at present in Canada and in the other jurisdictions in which Liquidnet's affiliates are active, please see Liquidnet Canada Trading Rules, section VI ("Targeted Invitations") (available at https://www.liquidnet.com/transparency-regulatory under the heading "Liquidnet Canada Trading Rules Summary").

[13] The exemptive relief order was necessary to address the pre-transparency requirement that would otherwise apply to the orders (i.e., the firmed-up "targeted invitations") that are communicated during the matching process; accordingly, much like Liquidnet, Cboe Canada is filing an application for exemptive relief for Directed IOIs in conjunction with this proposed change, as explained above in the section under the heading "Exemptive Relief from "Pre-Trade Transparency" Requirement."

[14] Cboe Europe Limited is a Recognised Investment Exchange regulated in the U.K. by the Financial Conduct Authority. Cboe Europe B.V. is a Regulated Market regulated in the Netherlands by the Authority for the Financial Markets. See, e.g., https://www.cboe.com/europe/equities/regulation/.